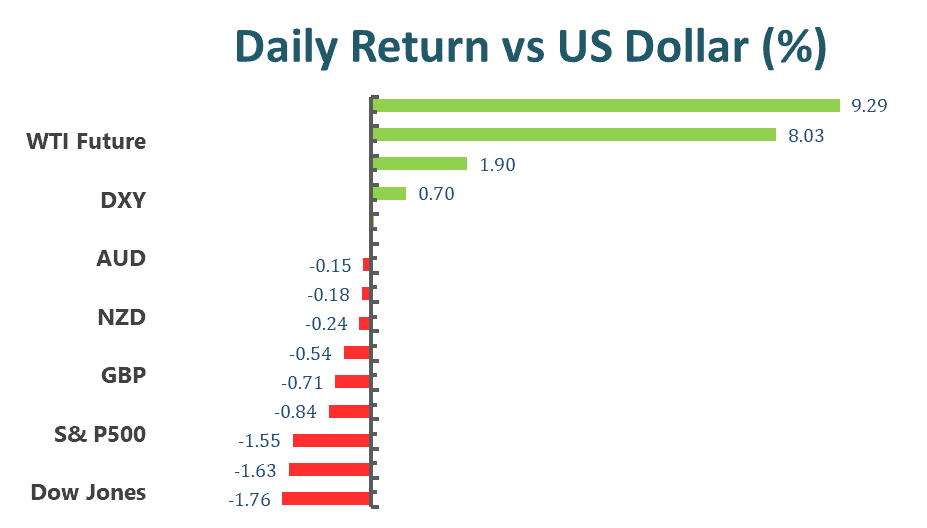

Wall street three major indexes ended sharply on Tuesday, with the bank stocks tumbled due to falling U.S. Treasury yields and worries about the economic outlook after oil rose above $100 a barrel as Russia ramped up its crackdown on Ukraine. At the end of the market, the Dow Jones Industrial Average fell 1.76% to 33,294.95 points, the S&P 500 index lost 1.55% to 4,306.24 and the Nasdaq Composite Index dropped 1.59% to 13,562.46 points. Not only U.S. stocks were under pressure, but so was Europe, with major stock indexes in Germany, France, Italy and Spain closing down more than 3%, while the pan-European STOXX 600 index fell 2.4%.

10 sectors in the S&P 500 ended lower, with the financial sector falling the most, down 3.71%, followed by material and information technology sectors, down 2.31% and 1.99%, respectively. The only winner is the energy sector, which has received a huge boost from skyrocketing oil prices. In the financial sector, regional banks including Silicon Valley Bank Financial Group, Zion Bank and Regional Financial Corporation lead the way financial stocks sold off as U.S. government yields, which dropped 7.94%, 5.95% and 8.60% respectively. Large-cap bank stocks were also hit hard, with JPMorgan Chase falling to a 52-week low, Wells Fargo and Bank of America down 5.77% and 3.91%, respectively. In the energy sector, APA Corporation, Chevron and Occidental Petroleum were among the top gainers, gaining 4.66%, 3.97% and 7.0%, respectively.

Main Pairs Movement:

Tension in Eastern Europe continue to lead financial markets. Safe-haven assets continued to rise as Russia escalated its attack on Ukraine, while President Vladimir Putin said the invasion would continue until he hit his target. Neutral countries have joined the global effort to stop Russia. Countries such as Switzerland and Finland are either sending armored vehicles to Ukraine or joining the financial blockade against Moscow. Meanwhile, the next round of talks between Russia and Ukraine will take place on Wednesday.

The dollar rose against most of its major rivals, especially Euro. EUR/USD fell to its lowest since June 2020 and closed around 1.11200, while GBP/USD is hovering around 1.3320. On the other hand, commodity-linked currencies were relatively strong, with AUD/USD hovering around 0.7300 ahead of intraday gains and ended little changed around 0.7250. USD/CAD edged higher to settle near 1.2735 amid stocks fell and ignored record crude oil prices.

The gold prices continued to surge and topped $1,950 an ounce intraday, and held most of its gains at the market close. In addition, oil prices surged to their highest level in seven years on concerns that the Russian war would affect supply. WTI was trading as high as $106.76 a barrel, while Brent was trading at $107.25.

Technical Analysis:

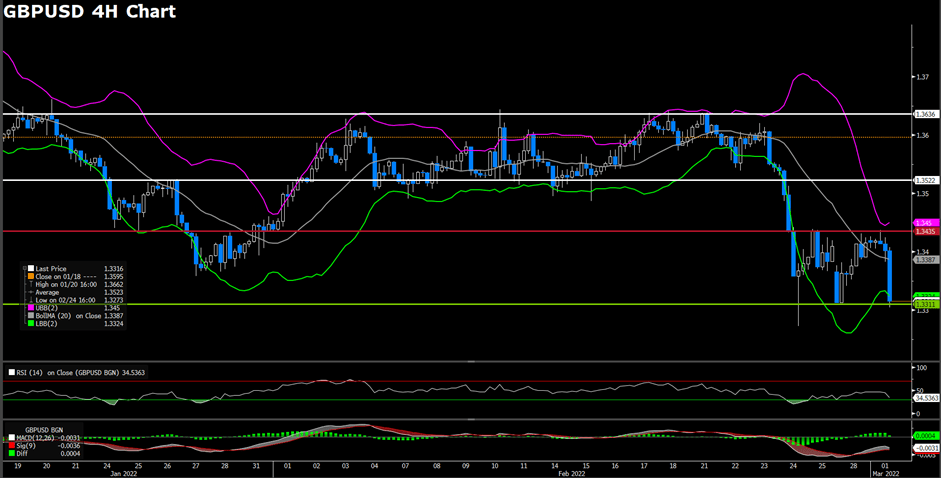

GBPUSD (4-Hour Chart)

Cable fell sharp against the greenback as market sentiment turned risk off once again. Ramping up sanctions from global economic power houses did not seem to yield expected results, as President Putin continues to increase military presence in Ukraine. The Dollar continues to to be the choice for risk hedging, however, Fed Chairman Jerome Powell is due to speak on the 2nd and could cause further price action for the Dollar.

On the technical side, Cable has fell through the short term support at 1.33722 and is consolidating around 1.3315, as of writing. RSI for Cable has dropped to 32.89, entering over-sold territory. GBPUSD is currently trading below its 50, 100, and 200 day SMA.

Resistance: 1.3435, 1.35212

Support: 1.331

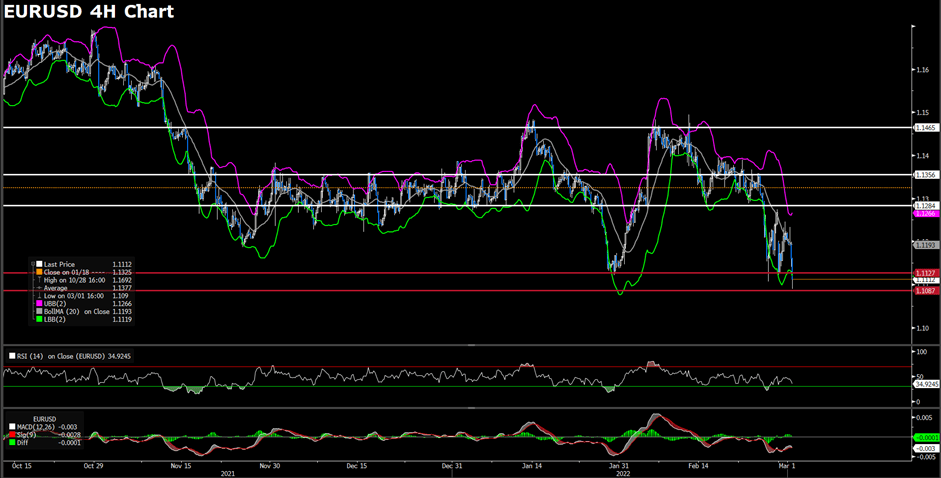

EURUSD (4-Hour Chart)

The Euro sank against the Dollar and the shared currency is projected to head even lower. With no foreseeable end to the Ukraine-Russia crisis, Europe’s energy crisis is being exacerbated as global financial sanctions pile on to Russia. Despite no direct sanctions on Russian energy exports as of yet, European nations still rely heavily on Russian energy exports, thus escalating uncertainty in Eastern Europe will continue to have spill-over effects on the European region and its currency; furthermore, the ECB’s unwillingness to raise interest rates only acts as a downward pressure on the shared currency.

On the technical side, EURUSD has broken below our previously estimated support level at 1.116. As of writing, EURUSD is consolidating around 1.1116. RSI for the pair is sitting at 33.31, indicating some over selling. EURUSD is currently trading below its 50, 100, and 200 day SMA.

Resistance: 1.1224, 1.12793

Support: 1.11629

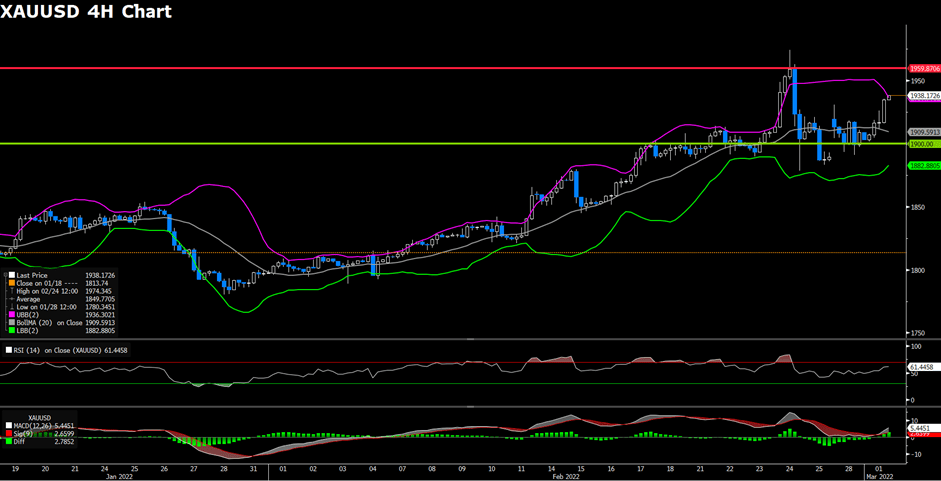

XAUUSD (4-Hour Chart)

Mounting tensions from the Ukraine-Russia crisis continue to send Gold prices higher. At the open of U.S. equity markets, Gold prices jumped 0.38% as market participants rotated into safe haven assets. However, the weaking U.S. treasury yield does not seem slow down the Dollar, evident from the Dollar index’s 0.77% intraday gain. As two of the world’s leading safe haven asset, Gold and the Dollar has recently exhibited highly correlated trading movements.

On the technical side, resistance levels for Gold seems to be irrelevant as any breaking news from Ukraine could send Gold flying through the resistance levels. Short term resistance level is projected at 1953 and Gold is firmly supported at the 1900 price level. RSI for XAUUSD is overheated at 71.49. XAUUSD is currently trading above its 50, 100, and 200 day SMA.