January 21, 2021

Daily Market Analysis

Market Focus

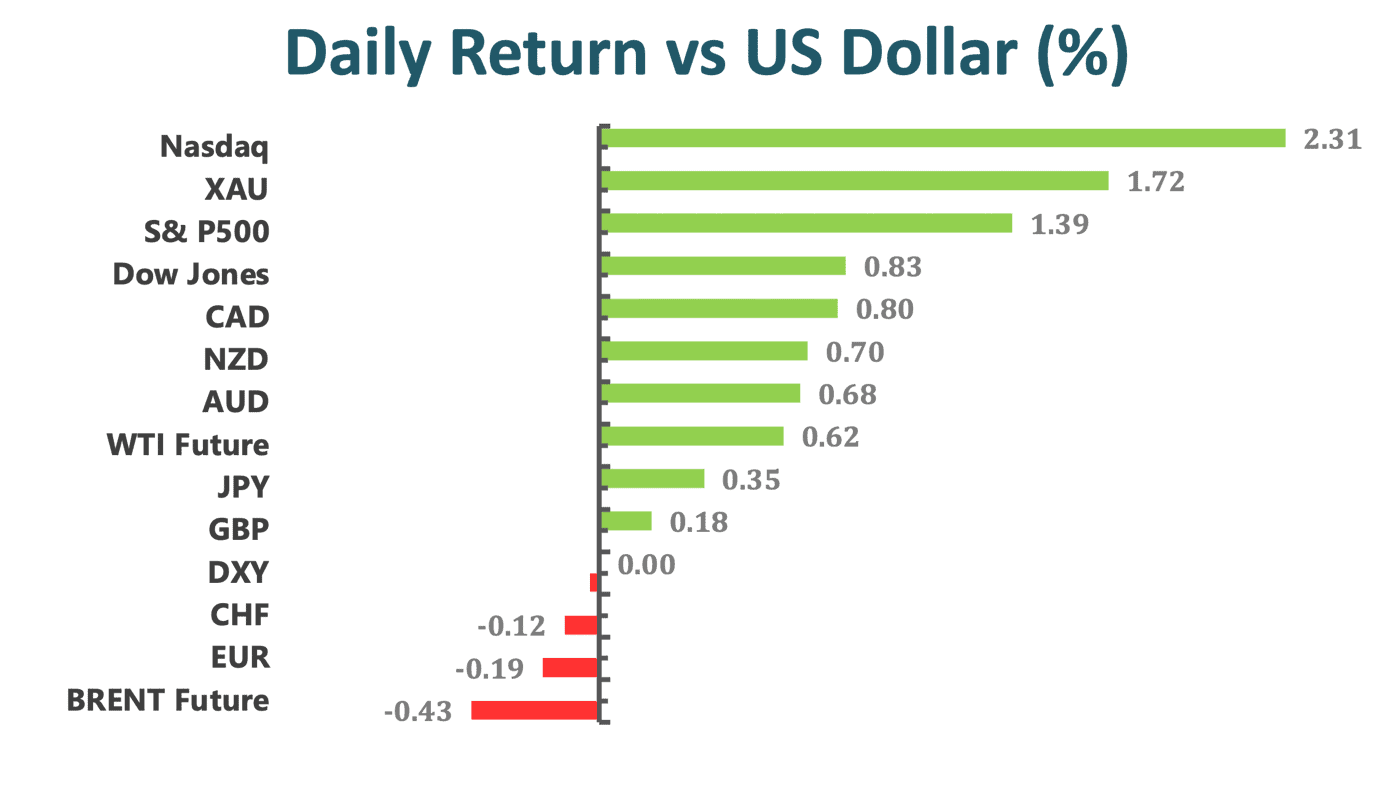

US stocks rallied to all-time highs as investors grew optimistic that recent federal spending will revive growth and bolster corporate earnings. Treasuries were little changed while the dollar weakened. The Nasdaq 100 Index jumped more than 2% and the SP500 Index posted the best first-day reaction to a newly elected president’s inauguration since Jan. 20 became the official start in 1937. Netflix Inc. surged more than 17% after a jump in subscribers. Chipmaker ASML Holding NV rallied on solid results. Morgan Stanley gained after reporting record full-year results.

Investors looked past a fresh stumble in the rollout of vaccines and elevated infection rates, and eyed the promise of more stimulus and an expanded federal effort to get shots to more Americans quickly under President Joe Biden.

According to Keith Buchanan, a portfolio manager for GLOBALT Investments, “If stimulus happens at the same time that people get vaccinated, the optimism can’t help but build. It’s a fairly safe bet there will be another stimulus package with more direct payments to consumers and individuals and more help for small businesses.”

While investors are counting on more spending to help propel economic growth under Biden, who is planning a flurry of executive orders on his first day, it won’t be all smooth sailing as Janet Yellen encounters early Republican resistance to Biden’s relief plan in her confirmation hearing to become Treasury Secretary.

Market Wrap

Main Pairs Movement

GBPUSD has fallen off the peak of 1.3719, the highest since 2018, amid fresh dollar strength. Optimism about the UK’s vaccine campaign and lower cases boosted sterling earlier. The greenback awaiting Biden’s first moves as President. The pair dropped from pre-release levels close to 1.2700 to nearly as low as the 1.2600 mark, before pairing losses to settle closer to 1.2650. In doing so, the Loonie hit its highest levels in nearly three years versus the US dollar. USDJPY resumed its decline after failing to advance beyond 104.00. Pressure mounts as investors await for Bank of Japan.

Crude Oil markets trade on the front foot on Wednesday, though have largely failed to take advantage of a recent improvement in risk appetite that has seen US stocks surge since the open and the US dollar fall, particularly against commodity FX. DXY met buyers in the 90.30 region earlier on Wednesday and now resumes the upside to the 90.50/55 band.

Technical Analysis:

EURUSD (4 Hour Chart)

After touching the lows around 1.2077 briefly, EURUSD has bounced back to near 1.21 as Biden becomes US President. Given that the EURUSD failed to extend its weekly recovery above the 1.2160 level and that the greenback has slightly bounced back on the Inauguration Day, the bears are attracted back to the market to undermine the prices of EURUSD. Markets are now focusing on how Joe Biden and his administration would address the ongoing trade conflict with China, the nuclear agreement with Iran, stimulus plans, and extra announcements regarding green energy.

Reflecting from the chart, it is inferable that the bulls have met some new contention around both 1.2160 and 1.2116 resistance level. Knowing that the EURUSD is currently trading above 1.21 (a relatively high price range in recent years), it is reasonable to believe that a strengthened USD and global economic prospects would continue to keep the pair on the back foot. On top of that, a bearish trend is also supported by both the 60-Day SMAVG and the MACD histogram. If the decline continues, the first cushion would be found near 1.2077, then 1.2054, followed by 1.1992.

Resistance: 1.2116, 1.2170, 1.2206

Support: 1.2077, 1.2054, 1.1992

AUDUSD (4 Hour Chart)

Even though the Aussie continued to rise and even staged a short-lived surge towards the 0.7761 resistance, the lack of a further USD losses still keeps the pair from penetrating the pair’s most immediate resistance. At the time of writing, the relatively weak greenback and the lifted risk appetite have contributed to the Aussie’s 3 consecutive day gains. The upcoming AUD Employment Change (Dec) is closely monitored, and a number that beats the markets expectation may provide the much-needed boost for the pair to top near the psychological resistance at 0.7798.

From a technical perspective, Aussie’s recent rise is not yet supported by SMAVG and MACD, but both indicators are staging a cross that would soon indicate a bullish trend. Additionally, as the RSI has been consistently rising to the high 50s, it is clear that the traders are placing their bets on the bulls. However, it would be not be prudent to place any long positions until further confirmative news solidify Aussie’s upward momentum.

Resistance: 0.7761, 0.7798

Support: 0.7705, 0.7663, 0.7634

XAUUSD (4 Hour Chart)

The Gold is now trading around 1870, nearing its most immediate resistance at 1871, amid the risk-on sentiment across the board as US President Joe Biden speaks in the US Inauguration Day. The greenback today has an uneven performance as investors eagerly wait for a catalyst given that the macroeconomic calendar had little to offer so far for this week. According to analysts at TD Securities, the reason why the gold is being pulled upward amid a market-wide risk-on sentiment is that the gold inherent inflation-hedging properties, which can successfully take care of investors’ concerns over rising inflation expectations. However, if the demand volume for the Gold recedes, the counter-inflation nature of the yellow metal could lose its position and value in the market. From a technical perspective, the short-term bullish momentum of the yellow metal is supported by the MACD and RSI reading. If the precious metal can penetrate the $1871 resistance level, the next resistance can be found at $1882, then $1891. On the flip side, the cushions for the pair are $1847, $1839, and $1823.

Resistance: 1871, 1882, 1891

Support: 1847, 1839, 1823

Economic Data

|

Currency

|

Data

|

Time (TP)

|

Forecast

|

|

AUD

|

Employment Change (Dec)

|

08.30

|

50.0K

|

|

JPY

|

BoJ Monetary Policy Statement

|

11.00

|

N/A

|

|

JPY

|

BoJ Outlook Report

|

11.00

|

N/A

|

|

JPY

|

BoJ Press Conference

|

11.00

|

N/A

|

|

EUR

|

Deposit Facility Rate (Jan)

|

20.45

|

-0.50%

|

|

EUR

|

ECB Interest Rate Decision (Jan)

|

20.45

|

N/A

|

|

USD

|

Building Permits (Dec)

|

21.30

|

1.604M

|

|

USD

|

Initial Jobless Claims

|

21.30

|

910K

|

|

|

|

|

|

USD

|

Philadelphia Fed Manufacturing Index (Jan)

|

21.30

|

12.0

|

|

|

|

|

|

EUR

|

ECB Press Conference

|

21.30

|

N/A

|

|

|

|

|