US stocks declined higher on Thursday, struggling for direction and saw a lot of instability near a key technical level as traders awaited the all-important jobs report for clues on the Federal Reserve’s next policy steps. The persistent optimism and tepid US data continued to support the Federal Reserve’s monetary policy pivot and dragged the US Dollar to multi-month lows.

The dovish bias of the Federal Reserve (Fed) Chairman Jerome Powell, as well as downbeat comments from US Treasury Secretary Janet Yellen, initially raised hopes of easy rate hikes. Additionally, some Chinese cities announced they are easing their testing and control coronavirus-related policies, which acted as a tailwind for the equity markets.

On Friday, the US will publish the Nonfarm Payrolls report, which might provide fresh impetus. On the Eurozone front, investors are waiting for the speech from European Central Bank (ECB) President Christine Lagarde.

The benchmarks, S&P 500 and Dow Jones Industrial Average both little changed on Thursday as the S&P 500 closed mixed but the US 10-year Treasury bond yields plummeted to a four-month low. The S&P 500 was down 0.09% daily and the Dow Jones Industrial Average dropped lower with a 0.6% gain for the day. Eight out of eleven sectors in the S&P 500 stayed in negative territory as the Financials sector and the Consumer Staples sector is the worst performing among all groups, losing 0.71% and 0.47%, respectively. The Nasdaq 100 meanwhile was little changed with a 0.1% gain on Thursday and the MSCI World index was up 0.8% for the day.

Main Pairs Movement

The US dollar slumped sharply on Wednesday, suffering from daily losses and dropped towards the 104.70 level amid expectations for the Federal Reserve’s monetary policy pivot. The dovish comments from Fed policymakers favouring a 50 bps Fed rate hike in December allowed the US Treasury bond yields to refresh a four-month low amid receding market pessimism and a rush toward the riskier assets. The focus will then shift to the release of the closely-watched US monthly jobs report – popularly known as NFP.

GBP/USD surged higher on Thursday with a 1.57% gain after jumping above the 1.2030s area as the US Dollar struggles to gain any meaningful traction. On the UK front, the overnight dovish remarks by Bank of England (BoE) Chief Economist Huw Pill failed to drag the cable lower. Meanwhile, EUR/USD regained upside traction and grinds near a five-month high past 1.0500 amid a weaker US dollar across the board. The pair was up almost 1.10% for the day.

Gold rallied sharply with a 1.96% gain for the day after refreshing a four-month high above the $1,800 mark during the US trading session, as the hopes of slower Federal Reserve rate hikes provided strong support to the precious metal. Meanwhile, WTI Oil advanced sharply with a 0.83% gain for the day.

Technical Analysis

EURUSD (4-Hour Chart)

The EURUSD extends its rally above the 1.0500 level following the release of US annual PCE inflation data and the ISM Manufacturing PMI. The data from the US showed the annual Core PCE Price Index declined to 6% in October and the ISM Manufacturing PMI dropped to 49.0 compared to the previous 50.2, triggering a fresh leg of US dollar selloff. Moreover, the US Federal Reserve Chair Jerome Powell dropped the hawkish rhetoric on monetary policy at a private event. Powell acknowledged that moderating the pace of rate hikes is the path to take and may come as soon as December, as progress towards “sufficiently restrictive” police has already been made. The dovish speech undermined the US Dollar situation, which, in turn, provide support for the pair. In the eurozone, German Retail Sales fell by 2.8% MoM in October, much worse than anticipated. Additionally, S&P Global released the final version of its November Manufacturing PMIs, which were downwardly revised. The German index was confirmed at 46.2, while the Euro Area one came down to 47.1 from the previously estimated 47.3. Despite discouraging news for the EUR, the upbeat mood keeps the pair afloat.

From the technical perspective, the four-hour scale RSI indicator surged to 68 figures as of writing, suggesting that the pair was surrounded upbeat market mood. As for the Bollinger Bands, the euro was pricing along with the upper band, and the size between upper and lower bands became larger, which is a signal that the pair would persist in its positive traction in the near term.

Resistance: 1.0604, 1.0774

Support: 1.0315, 1.0228, 0.9961

GBPUSD (4-Hour Chart)

The GBPUSD has preserved its upside traction and was trading around the 1.2250 level as of writing, with the softer-than-expected PCE inflation data and the disappointing ISM Manufacturing PMI weighing heavily on the US Dollar, fueling the pair’s upside. The monthly Core PCE price index declined to 0.3% in October and the annual fell to 6%, compared to the previous of 0.5% and 6.3%. Moreover, the ISM Manufacturing PMI in November fell below the 50 figure to 49.0. The economic data released on Thursday showed easing inflation signs and weakening conditions in the Manufacturing sector, which triggered mounting speculation about less hawkish rate hikes, pushing the greenback further lower. Apart from this, after the FOMC Chairman, Jerome Powell, reaffirmed that smaller rate hikes could come as early as December, the CME FedWatch Tool’s probability of a 50 basis points rate hike at the next policy meeting jumped to 80% from 66%. Powell further added that they have made substantial progress toward a “sufficiently restrictive policy,” further weighing on the USD. The US Dollar index was trading at 104.8 at the moment of writing.

From the technical perspective, the four-hour scale RSI indicator jumped to 70 figured as of writing, which has entered into an overbought zone, suggesting that a corrective pullback could be expected in the near term. As for the Bollinger Bands, the pair was priced above the upper band, and the size between the upper and lower bands get larger, meaning the bullish momentum would persist shortly.

Resistance: 1.2400, 1.2600

Support: 1.2154, 1.1927, 1.1765

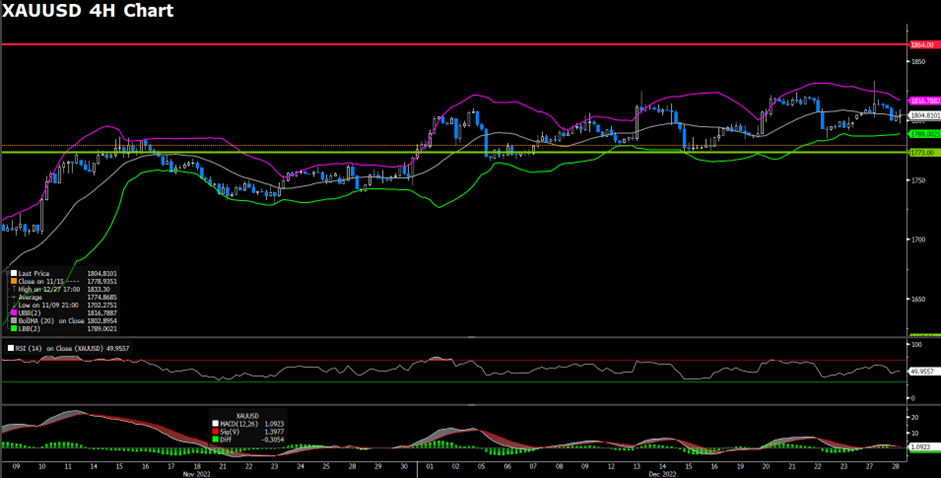

XAUUSD (4-Hour Chart)

The XAUUSD jumped above a critical psychological level of $1800, the highest since early August. The precious metal benefited from an extended USD sell-off as US macroeconomic figures fueled Powell’s triggered slump. On Wednesday, the Dollar fell on the back of a dovish message from Fed’s Powell.

The US Dollar remained under pressure throughout all day, extending its losses during the US trading session. On the one hand, the Personal Consumption Expenditures (PCE) Price Index rose by 6% YoY in October, easing from 6.3% in the previous month. In addition, core PCE inflation came in at 5% in the same period, down from 5.2% in September. On the other, the ISM Manufacturing PMI fell to 49 in November, down from the previous 50.2, being the first time the indicator signals contraction since the early stages of the pandemic. The events reflect the high risk of an economic setback after the US central bank aggressively hiked rates to tame inflation. Price pressures give signs of receding, although the risk of an economic downturn has increased.

From the technical perspective, the four-hour scale RSI indicator rose above 75 figures as of writing, suggesting that the pair was surrounded by strong upside momentum and the market mood. As for the Bollinger Bands, the pair was priced above and along with the upper band, and the gap between upper and lower bands became larger, signalling that the pair was more favoured to the upside path shortly.